Master Your Money: The Ultimate Guide to Home Household Finance Organizers

In an era of subscription fatigue and rising living costs, the traditional method of balancing a checkbook is no longer sufficient. Modern financial management requires a proactive approach, one that moves beyond simply recording transactions to actively forecasting and planning. This shift has given rise to a new generation of Home Household Finance Organizers. These are not merely lists of expenses; they are comprehensive systems designed to bring clarity to the chaos of domestic economics. For families, couples, and individuals, utilizing a structured organizer is the first step toward financial sovereignty.

The Evolution of Domestic Budgeting

Historically, household finance was a reactive practice. You earned money, spent it, and hoped there was enough left over at the end of the month. Today, the landscape is far more complex. The average household juggles multiple income streams, numerous subscription services, variable utility rates, and fluctuating grocery prices. Consequently, the tools we use must evolve. Home Household Finance Organizers have transformed from simple ledgers into dynamic dashboards. They reflect a lifestyle where financial literacy is not just a skill for the wealthy, but a necessity for everyone aiming to build stability in an unpredictable economy.

Why Spreadsheets Remain the Gold Standard

While dedicated banking apps offer convenience, they often lack the granular control required for true financial planning. This is where Home Household Finance Organizers Spreadsheet Templates in Excel Google Sheets shine. These platforms offer a perfect balance of structure and flexibility. Unlike rigid apps, a spreadsheet template allows you to customize categories, adjust formulas to fit your specific tax situation, and visualize data exactly how you see fit.

The use of Home Household Finance Organizers Spreadsheet Templates in Excel Google Sheets has surged because they bridge the gap between automated banking and manual oversight. When you input data manually or review it in a spreadsheet, you engage with your money on a psychological level that "set and forget" apps cannot replicate. This engagement is crucial for changing spending habits and adhering to long-term goals.

Anatomy of an Effective Finance Toolkit

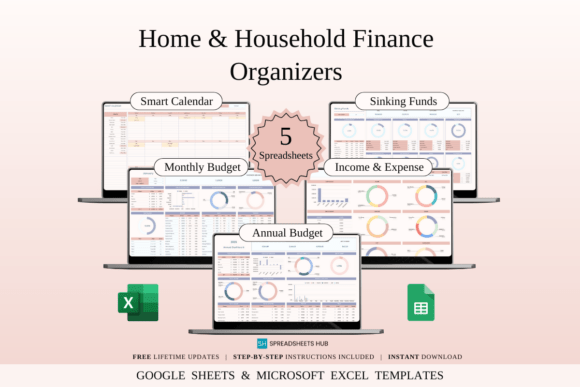

A robust organizer is more than a single list. It is a collection of tools that work in harmony to provide a holistic view of your finances. A high-quality toolkit, such as the Household Budget Finance Toolkit, typically includes several distinct components, each serving a specific purpose in your financial lifecycle.

The Annual Budget Planner

Long-term vision is the cornerstone of wealth building. An Annual Budget Planner allows you to map out the entire year in advance. This is essential for anticipating "lumpy" expenses—costs that do not occur monthly but significantly impact your cash flow, such as property taxes, insurance premiums, or annual subscriptions. By forecasting these expenses, you can set realistic savings goals and avoid the shock of large bills when they arrive.

The Monthly Budget Sheet

While the annual view provides the roadmap, the Monthly Budget Sheet is the vehicle that gets you there. This component breaks down your income and expenses into manageable, bite-sized pieces. It allows you to track variable spending categories like dining out, entertainment, and groceries. By reviewing this sheet monthly, you can identify patterns—perhaps you are consistently overspending on takeout in the third week of the month—and make immediate adjustments.

Bill Payment Calendar

Cash flow timing is often the hidden culprit behind financial stress. You might have enough money to pay your bills, but if they are all due on the same day, you risk overdrafts. A Bill Payment Calendar visualizes your obligations chronologically. Seeing that the car insurance is due on the 15th and the mortgage on the 1st allows you to align your paychecks with your outflows, ensuring liquidity throughout the month and eliminating late fees.

Income and Expense Tracker

For freelancers, gig workers, or anyone with irregular income, an Income Expense Tracker is indispensable. This tool monitors the flow of funds in real-time. It serves as a reality check, comparing what you planned to spend with what you actually spent. Over time, this data becomes invaluable for tax preparation and for understanding your true net worth.

Sinking Funds Organizer

One of the most practical features of modern organizers is the Sinking Funds Organizer. This concept involves setting aside small amounts of money regularly for specific future expenses, such as a vacation, a new car, or holiday gifts. Rather than putting these purchases on a credit card and paying interest later, a sinking fund ensures the cash is ready when the need arises. It transforms large, scary expenses into manageable monthly line items.

Who Benefits Most from These Tools?

The utility of Home Household Finance Organizers extends across various demographics and life stages. They are particularly effective for:

- Families and Couples: Managing shared finances requires transparency. A shared spreadsheet template ensures both partners are on the same page regarding spending limits and savings targets.

- Homeowners: Property ownership comes with a myriad of variable costs, from maintenance to HOA fees. An organizer helps track these specific housing-related expenses separately from general living costs.

- Freelancers and Entrepreneurs: When your income varies, budgeting based on a fixed salary is impossible. These organizers allow for flexible budgeting that accommodates high-earning months and lean periods.

Integrating Organizers into Modern Workflows

The modern workflow is digital and mobile. Home Household Finance Organizers Spreadsheet Templates in Excel Google Sheets fit seamlessly into this environment. Google Sheets, for instance, allows for real-time collaboration. A couple can update the grocery budget from their phones while at the store, and the changes instantly reflect on the home computer. Excel offers powerful offline capabilities and advanced data analysis features for those who prefer a desktop-centric approach. The key is accessibility; your budget should be available wherever you make financial decisions.

Practical Tips for Implementation

Purchasing or downloading a template is only the beginning. To truly master your finances, you must implement the system effectively.

- Schedule a Weekly Review: Set aside 15 minutes every Sunday to update your tracker and review the upcoming week's expenses.

- Be Specific with Categories: Avoid vague categories like "Miscellaneous." Instead, create specific categories like "Pet Care" or "Home Maintenance" to get actionable insights.

- Embrace the Sinking Fund: Start small. If you know you need $600 for holiday gifts, set aside $50 a month starting in January. By December, the money is there without the financial strain.

- Review and Adjust: A budget is a living document. If you consistently fail to meet a specific target, analyze why. Is the goal unrealistic, or is the spending habit too ingrained? Adjust the budget or the behavior accordingly.

The Psychological Shift: From Stress to Control

Ultimately, the goal of using Home Household Finance Organizers is not restriction, but liberation. Financial anxiety often stems from the unknown. When you don't know where your money is going, every unexpected expense feels like a crisis. By bringing your finances into the light—organizing them into clear, manageable categories—you replace fear with knowledge.

This shift allows you to make proactive choices. Instead of wondering if you can afford a spontaneous weekend getaway, you can check your "Travel Sinking Fund" and know immediately. Instead of panicking about a tax bill, you can refer to your Annual Planner where the funds have been accumulating. Home Household Finance Organizers Spreadsheet Templates in Excel Google Sheets provide the framework, but the true value lies in the peace of mind and financial confidence they cultivate. By adopting these tools, you are not just organizing numbers; you are designing a more secure and intentional future for your household.